Over the last decade, I’ve noticed a theme when working with my client families. While the question may not come out exactly this way, the essence usually distills to, “How should we allocate our hard-earned dollars?” One of the key concepts in financial management is cash flow – the inflow and outflow of money in your life. This guide will explore making the most of every dollar you earn by strategically allocating it to various financial goals and objectives.

Cash Flow Optimization in 10 Steps: Make Every Dollar Count

What is Cash Flow?

Personal cash flow refers to the movement of money in and out of your financial life over a specific period, typically a month or a year. It encompasses the income earned from various sources, such as salaries, investments, and side hustles, as well as the expenses incurred for daily living, financial obligations, and discretionary spending. The concept emphasizes the balance between income and expenditures, reflecting whether your finances are in a surplus or deficit. Effective management involves optimizing income, minimizing expenses, and strategically allocating funds toward financial goals, savings, investments, and debt repayment. By understanding and controlling where your money comes and goes, you can achieve financial stability, meet your financial objectives, and make informed decisions about your financial future.

Cash Flow Statement

A personal cash flow statement is a financial document that provides a comprehensive overview of your income, expenses, and savings over a specific period, usually a month or a year. It tracks the movement of money into and out of your financial life, allowing you to understand your financial inflows, outflows, and what’s left.

This statement typically consists of three main sections:

- Income:

This section lists all sources of income, such as salaries, wages, bonuses, rental income, dividends, and any other money received. It provides a clear picture of how much money is coming in during the specified time frame.

- Expenses:

Here, all expenses are categorized and listed, including fixed expenses (like rent or mortgage payments), variable expenses (such as groceries and entertainment), and discretionary spending (like dining out or shopping). Tracking expenses helps you understand where your money is going and identify potential areas for savings.

- Savings and Net Cash Flow:

This section calculates the difference between total income and total expenses, resulting in the net cash flow. If the result is positive, it means you’re saving more than you are spending, which is a healthy financial situation. If the result is negative, it indicates that you are spending more than you are earning, which may require adjustments to your financial habits.

Creating and regularly updating a statement like this is a valuable financial practice. It can help you make informed budgeting, saving, investing, and debt management decisions. By understanding your spending patterns, you can take control of your finances, align your spending with your goals, and work towards achieving greater financial stability and success.

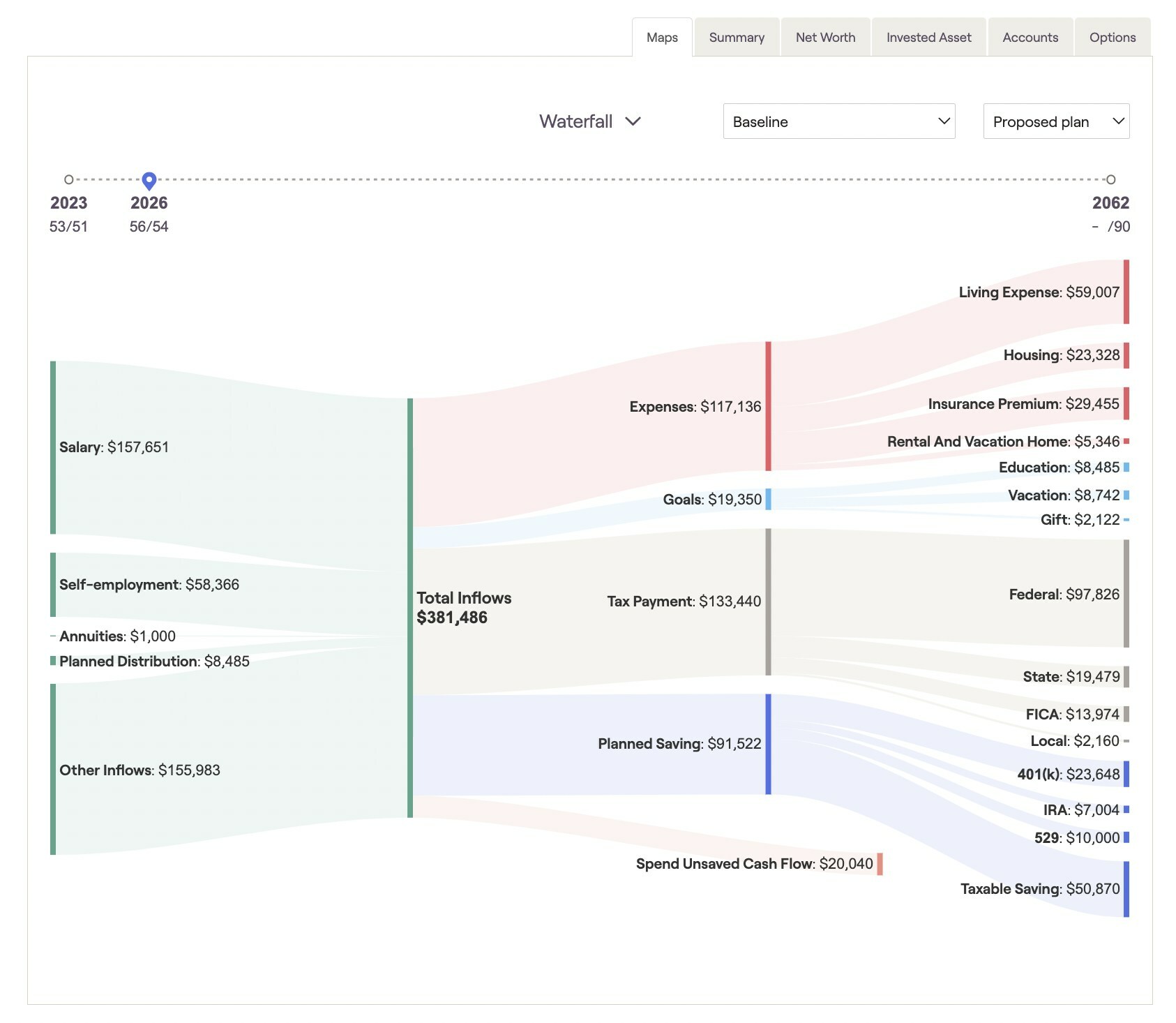

This “Waterfall” visual is a sample of the cash flow analysis we use with our client families, showing cash inflows and outflows.

Cash Flow Optimization in 10 Steps

Step 1: Assess Your Cash Flow Plan

Before diving into the world of investments and savings strategies, ensuring that your financial foundation is solid is essential. Adequate emergency funds, manageable debt, and appropriate insurance coverage are the cornerstones of a strong financial base. A robust foundation provides peace of mind and safeguards your cash flow from unexpected financial shocks.

Step 2: Leverage Your Employer Benefits

Employers often offer a range of benefits that can contribute significantly to long-term savings. These benefits can include matching contributions to retirement accounts, Employee Stock Purchase Plans (ESPP), and more. By taking advantage of these opportunities, you get “free money,” which can substantially boost your overall cash flow. Make sure to understand and maximize these benefits to their fullest extent. Keep in mind any restrictions and time-sensitive considerations associated with these benefits. A strategic approach ensures you maximize your income while adhering to your financial goals.

Step 3: Define Your Primary Financial Goals Through a Cash Flow Lens

A clear goal should drive every financial decision. Whether you’re saving for retirement, a specific expense, or a broader financial planning objective, understanding your primary goal is crucial. Aligning your financial decisions with this goal ensures that your cash flow is directed toward achieving tangible results that matter to you.

Step 4: Consider the Tax Implications of Your Current Cash Flow

Tax planning plays a pivotal role in optimizing where to save your money. Depending on your circumstances, you might prefer tax flexibility now or in the future. This decision involves considering whether you expect your future taxes to be equal to or higher than your current taxes. Balancing immediate tax benefits with long-term considerations is a key aspect of effective cash flow management.

Step 5: Evaluate Retirement Saving Strategies

Saving for retirement is a common long-term goal for many individuals. Retirement accounts like IRAs and 401(k)s offer tax advantages but come with withdrawal limitations. These accounts can significantly impact your cash flow during retirement, so carefully evaluate your comfort level with restricted access versus the tax benefits they provide.

Wondering how to optimize your budget? Use our handy flowchart “Where Should My Next Dollar Go?”

Step 6: Balance Short-Term and Long-Term Cash Flow Needs

While long-term goals are essential, balancing saving for tomorrow and living for today is crucial. If you foresee needing funds within the next five years, prioritize liquidity and stability. Maintaining an equilibrium between these needs ensures that your money remains flexible and adaptable.

This is the part of the process where you take what you learned in the first five steps and use that information to create a budget. If the words ‘create a budget’ make you cringe, don’t worry. This rule of thumb might help:

-

The 50/30/20 Rule

This guideline suggests allocating 50% of your income to needs (essential expenses like housing and utilities), 30% to wants (discretionary spending like entertainment and dining out), and 20% to savings and debt repayment (building an emergency fund, saving for goals, and paying off debts). This rule helps individuals create a balanced budget that addresses immediate necessities and long-term financial objectives.

Of course, “mileage may vary,” and this may not be the right strategy for you. Your best bet is to sit down with a fee-only Certified Financial Planner™ professional to co-create the right strategy for you. You can learn more about creating a budget by checking out this article by our friends at Nerd Wallet, Budget 101: How to Budget Money.

Step 7: Anticipate Future Tax Scenarios

Understanding potential future tax scenarios is essential for effective financial planning. Assessing whether your future taxes will be equivalent to or greater than your current taxes helps you make informed decisions about when to pay taxes. This anticipation can influence the timing of your financial moves and their impact on your cash flow.

Step 8: Choose Goal-Specific Accounts for Cash Flow Planning

Different financial goals often align with specific types of accounts. Health Savings Accounts (HSAs) are ideal for medical expenses, while 529 plans are tailored for educational goals. However, these specialized accounts may have liquidity issues and penalties. Evaluating these limitations against your budgetary requirements is vital before committing to them.

Step 9: Align Cash Flow with Planning Strategies

Financial planning strategies, such as Roth conversions, legacy funding, and debt payoff, can significantly impact your cash flow. The key is to feel comfortable with these strategies, even if they affect your liquidity. Weigh the long-term benefits against short-term limitations to ensure your chosen strategies support your financial well-being.

Step 10: Tailoring Your Investment Choices

Investing plays a crucial role in enhancing your cash flow over time. Assess your risk tolerance and liquidity needs when selecting investment options. Low-volatility assets like bonds and CDs provide stability, while higher-growth assets like equities offer long-term gains. Balancing these choices is essential for optimizing your budget while managing risk.

In Closing…

In a world filled with financial opportunities and challenges, understanding how to allocate your money effectively is paramount. You can optimize your short- and long-term cash flow by assessing your financial foundation, leveraging employer benefits, defining your goals, considering tax implications, and aligning with effective planning strategies.

Consistency is the biggest struggle I see for folks trying to maintain a budget. It’s hard to maintain transaction tracking long-term. The more you can automate both savings and spending, the better. You can learn more about the handy way we do that here at Collective Wealth Planning by visiting our blog: Cash Flow Plan: How to Create One.

Remember, every dollar has the potential to contribute to your financial well-being and bring you closer to your dreams. By mastering the art of strategic allocation, you’re not just managing money – you’re managing your money for a brighter financial future. Want a thought partner on your unique situation and co-create a plan for you? Reach out; I welcome the conversation.

FAQs About Cash Flow

-

What is a cash flow statement?

- A cash flow statement is a financial report that summarizes the inflows and outflows of cash within your finances over a specific period, helping to track the sources and uses of cash.

-

Why is a cash flow analysis important?

- A cash flow analysis empowers you to understand your financial health by tracking the movement of money in and out, helping you make informed decisions, manage liquidity, and ensure sustainable operations or financial stability.

-

How is a cash flow statement prepared?

-

A cash flow statement like this is prepared by documenting all sources of income and categorizing expenses over a specific period, subtracting expenses from income to determine net cash flow. This provides a clear overview of your financial inflows, outflows, and savings.

-